I must have missed something. Of course, with my 24-hour intensive care, it's almost impossible to avoid that a nurse notices what I do all day long. And since I unfortunately don't know any way of releasing a TAN with just my eyes, my carers are allowed to do it for me. I can't blame anyone when the embarrassed question follows whether we have just bought Lufthansa shares for €25,000.

What can I say? Yes? Men just never grow up. Only the toys get more expensive.

What has irritated me a little, however, is how often I have been asked recently to recommend an investment. I'm only talking about specific cases where I've been told concrete facts and possible investment sums. And many more private-confidential details that I didn't even ask for. And never would have. What a lot you entrust me with. Too much information.

And anyway, do I look like a financial advisor? No offense. But seriously, would you get investment advice from me? A guy,

- who smokes medicinal weed every day,

- who lies in bed all day,

- in whose condition flying would be even easier than walking,

- who bets for money,

- who bets for money and

- who pushes around shares for tens of thousands a month?

Reason? Does everything always have to have a reason? Well, because. Because he can. And because success and failure are so close together there that the thrill gives me a kind of satisfaction. You could also say in simple language, I enjoy it. Like this.

That's why the answer I give when asked for my opinion on various investments is not very scientific. I'll tell you, you obviously don't earn as badly as is often claimed in care. And sure, I'm happy to give you my thoughts on that. But I must clearly point out that this is only my opinion. I will never give financial advice. I don't have the training for that and besides, it's far too boring for me. So, anything that slips out of my mouth in this respect, you may take as my own personal opinion. Without liability and completely made up out of thin air. And hung with Siemens air hooks.¨#Insider.

So, my opinion on investments. It's really difficult at the moment because there is no reliable investment option that can compensate for inflation. Even with real estate it might just work. But only up to a certain point.

Fixed-term deposit

If you want something reliable, the Sparkasse is currently offering 2.1% on a fixed-term deposit with a term of twelve months. That won't knock your socks off. I know it won't. But it's the best I've seen from a bank in three years. It's just something for lazy, indecisive and risk-averse investors. One year is a manageable period of time, you don't need any investment skills at all and don't have to worry about it. In this respect, it is even interesting in a portfolio mix to reduce the overall risk.

ETF on the DAX

In my opinion, if you want more return, you have to sacrifice safety. Even with a 100% investment in DAX stocks, history and stochastics tell you that sooner or later you will suffer a severe price collapse. In the worst case, you will also experience the next financial crisis. You don't have to look far back to see what it's all about. Just think of the energy crisis, Russia's war of aggression on Ukraine and of course COVID-19 (Corona). But - and here I find applied mathematics mega exciting - with an ETF on the DAX you can't lose statistically for a duration of at least (I think) 13 years, history repeats itself unfortunately. As I said, belief is not knowledge. If you're interested in more detail, leave me a comment and I'll research a reliable source. What is certain is that with a ten-year investment period you will make a profit with 88% probability - taking crises into account.1https://www.boerse.de/grundlagen/aktie/Anlagehorizont-Langfristige-Investments-bieten-hoehere-Erfolgschancen. In my opinion, this is a calculable risk, because in the worst case, one would have to stay invested a few years longer after the last lean period. If that's not enough, then we'll probably all have completely different problems.

Investing in a secure fund on the DAX certainly appeals to the mathematician in me. And hey, I have a Bavarian 15-point maths Abi. I have a bit of an idea what I'm talking about (in case that doesn't mean anything to you, that's the top grade in the undisputedly most difficult final exams in German schools #KeinerMagSchlauberger ). But it's not really fun, there's nothing to do.

Shares

It may surprise some people, but I myself am currently only directly invested in shares. The Spielking doesn't like ETFs and other funds. It's only really fun to maintain your own portfolio of shares. I want to see where I'm invested and how much. I invest exclusively in companies whose ethics are at least halfway compatible with my world view. I can be completely wrong and invest in "Oatly" and practically ruin the whole thing. According to all the rules of stock theory, I should have gotten out long ago. But I don't. Because for me it is an ideological investment. Okay, next basic rule of the stock market broken, never get sentimental. Emotions have no place in the stock market. I'm just not the typical investor. But I want to sleep at night with a clear conscience and I can afford it. I could never invest in a Nestlé company, for example, or in mineral oil companies. I don't care about the profit outlook.

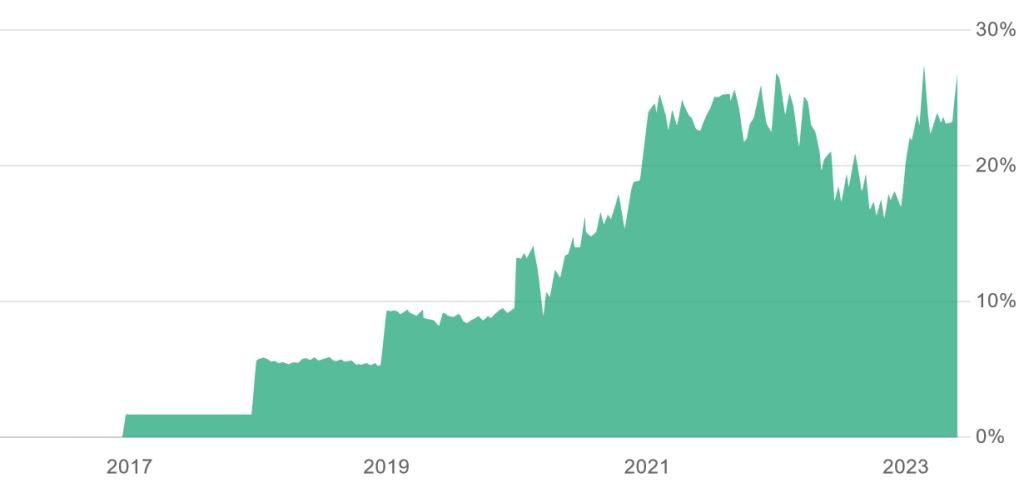

And at the end of the day, my success is fine. All joking aside, it took me a few years to get the hang of it. I didn't just take every crisis that was even remotely possible. No, I also really dug my heels in on the "Wirecard" whodunit. Shocked by the fact that my shares, which were once quoted at around €200, lost more than half their value, I struck again at around €85. Every textbook advises you that the only sensible thing to do is to keep losses low and get out immediately.

And if you take all that into account, I think the performance is actually quite fat. Show me another investment with comparable risk that makes 15% plus even in the worst of times.

But as I said, it's just my opinion. If you want to be reliably taken for a ride, ask your bank advisor about investment opportunities. He'll probably recommend a fund that's "absolutely safe", "outperforms" and, incidentally, earns your financial advisor more than you do. Wink Smiley